Risk Allocation in PPP Projects: Principles & Best Practices

Learn how risk allocation in PPP projects impacts bankability and bidding. Master the risk matrix and navigate India's unique infrastructure frameworks.

Every Public-Private Partnership hinges on a single question: who bears what risk? Get the answer wrong, and a project that looks viable on paper collapses under cost overruns, litigation, or outright abandonment. Get it right, and both the government authority and the private concessionaire walk away with a deal that's bankable, buildable, and fair. Risk allocation in PPP projects is the mechanism that determines this outcome, and for infrastructure firms bidding on roads, bridges, metro corridors, or urban development contracts across India, understanding it is non-negotiable.

The challenge is that risk allocation isn't a one-size-fits-all formula. It shifts based on project type, sector regulations, state-level procurement norms, and the specific concession agreement drafted by the contracting authority. A poorly structured risk matrix can saddle a private partner with force majeure liabilities they can't insure against, or leave a public authority exposed to demand risks it never anticipated. Identifying these red flags early, ideally before you commit resources to a bid, separates firms that grow strategically from those that burn capital on unwinnable contracts.

This is exactly why we built Arched. Our platform parses tender and concession documents automatically, flagging unusual risk clauses and qualification criteria so your BD team can evaluate exposure before deciding to bid. Instead of spending hours reading through dense PDFs, you get a clear picture of what a contract actually demands. In this article, we break down the core principles of PPP risk allocation, walk through common risk categories and who should own them, and outline the best practices that make projects fundable and executable.

Why risk allocation matters in PPPs

When a government authority signs a concession agreement with a private firm, both sides are making a long-term bet on outcomes they cannot fully control. Risk allocation in PPP projects determines who absorbs the financial consequences when those outcomes deviate from the plan, whether that is a construction cost blowout, a shortfall in traffic demand, or a change in government policy. For firms bidding on infrastructure contracts in India, this matters in a direct and immediate way: the terms embedded in the concession document define your exposure before you even break ground.

The cost of getting it wrong

A poorly structured risk allocation does not just reduce returns; it can end a project entirely. India's highway sector has produced clear evidence of this. When private developers took on aggressive demand risk during the early BOT-Toll wave without adequate traffic study support or termination payment provisions, many concessionaires faced financial distress within a few years of operations. Lenders withdrew, projects stalled, and the government eventually had to restructure dozens of contracts under NHAI's asset monetization framework. The core problem was not the project itself but the fact that risks were pushed to the party least capable of managing them.

Poor risk allocation does not just hurt the private partner; it delays public infrastructure delivery for years, which makes it a policy failure, not just a commercial one.

Understanding where your firm sits in this risk chain is essential before you commit to a bid. If a concession document places demand risk entirely on you without minimum revenue guarantees, or assigns utility shifting costs to the concessionaire without a clear timeline from the authority, you need to model the worst-case exposure before pricing your bid.

How proper allocation unlocks project finance

Infrastructure lenders and equity investors do not evaluate PPP projects the same way an engineering team does. Banks and institutional investors assess whether the risk structure makes a project's cash flows predictable enough to service debt. When risks are allocated to the party best positioned to manage them, the revenue stream becomes more reliable, and lenders can underwrite the project with reasonable confidence.

This is why government guarantees, termination payment mechanisms, and change-in-law provisions exist in well-structured concession frameworks. They signal to financiers that the project will not collapse the moment an external shock hits. For your firm, this means understanding risk allocation is not just a legal exercise; it directly determines whether you can raise the debt and equity needed to execute a contract.

What this means for your bidding strategy

Your bid strategy has to account for risk-adjusted returns, not just headline contract values. A contract worth INR 500 crore with unmanageable demand risk and no termination payment clause may deliver far worse outcomes than a smaller contract with well-defined risk sharing and guaranteed minimum revenue. Identifying the risk profile of a tender before you allocate bid resources is one of the most important filters your business development team can apply.

Applying this filter consistently across your pipeline is where most firms struggle. Reviewing dense concession documents manually takes time, and the risk clauses that matter most are often buried in annexures or referenced through secondary documents. Building a process to catch these clauses early is what separates firms that bid strategically from those that price risk by instinct.

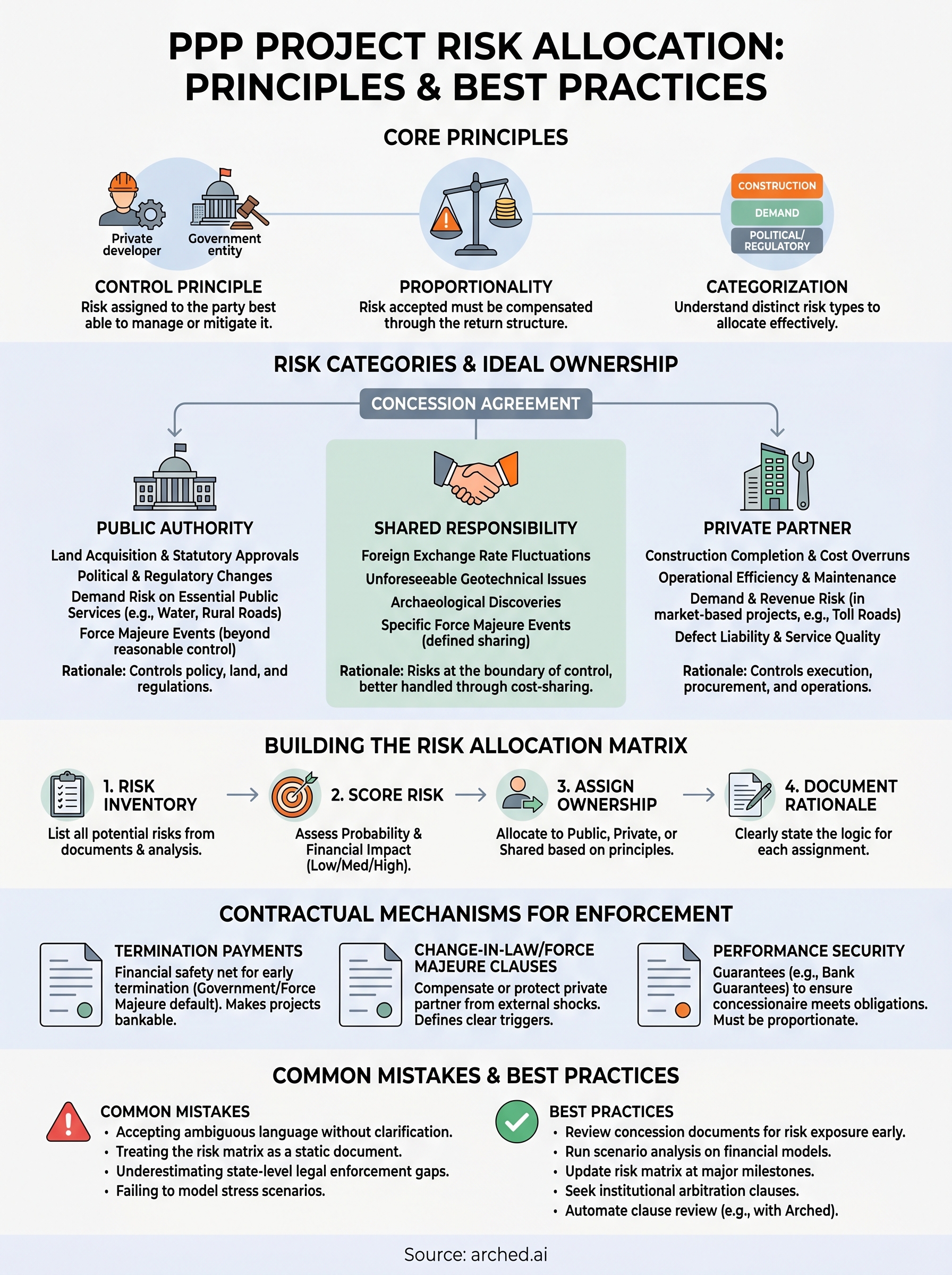

Core principles of PPP risk allocation

The entire discipline of risk allocation in PPP projects rests on a handful of principles that apply across sectors, geographies, and deal structures. These principles are not abstract theory; they are practical rules that determine whether your concession agreement will survive contact with lenders, insurers, and reality. Before you analyze a specific contract's risk matrix, you need to internalize these foundations so you can recognize when a draft concession document violates them.

Assign risk to the party best able to manage it

Effective PPP risk structuring starts with one rule: the party that has the most control over a risk, or the best tools to mitigate it, should carry it. A private developer has strong control over construction methods, material procurement, and project scheduling, so construction completion risk belongs with the concessionaire. A government authority controls the regulatory environment, land acquisition timelines, and policy decisions, so those risks belong on the public side of the ledger. Neither party should carry what the other is structurally better positioned to manage.

When risk is pushed to the party that cannot control or hedge it, the project's cost of capital rises, bid prices inflate, and the deal becomes harder to finance.

Violations of this principle appear regularly in state-level PPP documents in India, where land acquisition risk is sometimes transferred entirely to the private partner despite the authority having sole statutory power to acquire land. If you see this pattern in a concession document your firm is reviewing, model the delay scenarios carefully before you price the bid, because a six-month land acquisition delay can erode a project's returns significantly.

Risk must be proportionate to return

Every risk a private party accepts should be compensated through the return structure built into the concession. If you are taking on demand risk with no minimum revenue guarantee, your expected equity return must be high enough to justify the downside scenario. Concession agreements that impose wide risk transfer without a corresponding return premium create adverse selection, where only under-resourced or overconfident bidders submit proposals, which ultimately undermines project quality and delivery.

Checking whether your internal rate of return assumptions hold under stress scenarios is essential during bid preparation. Test what happens when demand falls 20% below projections or when construction costs rise by 15%. If the financial model breaks at those inputs, the risk-return balance is misaligned and your firm needs to either reprice or walk away from the bid entirely.

The main PPP risk categories to allocate

Before you can assign responsibility or build a risk matrix, you need to know what you are actually allocating. Risk allocation in PPP projects operates across several distinct categories, each with its own drivers, mitigation tools, and typical ownership patterns. Firms that conflate these categories during bid analysis often miss specific clause-level exposures that only surface once construction is underway or operations begin.

Construction and completion risk

This is the risk that a project will not be delivered on time, within budget, or to the specified technical standard. Construction risk sits predominantly with the private partner in most PPP frameworks, because the concessionaire controls procurement, workforce management, and site execution. What you need to watch for is how the concession document handles cost escalation triggers and force majeure carve-outs during the construction phase. Some agreements allow limited cost pass-through for defined events; others do not, which changes your contingency budgeting significantly.

The key construction risk exposures to verify in any concession document include:

- Liquidated damages caps and whether they are proportionate to delay scenarios

- Defect liability periods and the cost of remediation

- Approved subcontractor requirements that limit your procurement options

Demand and revenue risk

Demand risk is the possibility that actual usage, traffic volumes, or service uptake falls below the projections used to build the project's financial model. In toll road concessions, this risk responds strongly to competing routes, fuel prices, and regional economic activity. Some concession structures shift this risk to the government through Viability Gap Funding or minimum revenue guarantees, while others place it entirely on the concessionaire. Which of the two applies is decided by the contract model itself — HAM removes traffic risk while BOT retains it, and that single distinction changes how you underwrite the bid.

A single demand shortfall of 20% in year one of operations can push a project's debt service coverage ratio below the threshold lenders require, triggering covenant breaches before you have recovered construction costs.

Your financial model needs to run demand stress tests before you finalize your bid price. If the model breaks at a 15% to 20% shortfall with no guarantee backstop, the risk-return balance in that tender does not work for a privately financed project.

Political, regulatory, and land acquisition risk

These risks cover changes in law, policy shifts, and delays in statutory land acquisition. In the Indian context, land acquisition deserves its own attention because delays regularly stretch from months to years, yet some state-level agreements transfer this risk to the private partner. Termination payment clauses and change-in-law provisions are the primary contractual tools protecting a concessionaire when the government's own administrative actions disrupt project delivery. If these clauses are absent or weak, your exposure on a long-tenure concession is substantial.

Who should take which risks in a PPP

The question of who carries what risk is not a negotiation tactic; it is a structural decision that determines whether risk allocation in PPP projects produces a deal that is fundable and executable. Ownership of each risk category should follow the control principle: the party with the greatest ability to influence the outcome should hold the corresponding liability. Misassigning risk, whether through aggressive negotiation or template contracts that ignore project specifics, produces a deal that looks signed but fails in execution.

Risks the public authority should own

The government side of a PPP controls factors that no private firm can influence through better management or technology. Land acquisition timelines, statutory approvals, and changes in law fall squarely in this category because they depend entirely on the authority's administrative and legislative power. Transferring these risks to a concessionaire does not make them disappear; it forces the private partner to price them into the bid, which drives up project costs for the public.

When a concession agreement assigns land acquisition risk to the private partner despite the authority holding all statutory acquisition powers, lenders treat the project as structurally risky, which raises the cost of debt.

The public authority should also retain demand risk on essential public services where political constraints prevent realistic user charging, such as water supply or rural road concessions. In these cases, the government covers revenue shortfalls through availability payments or minimum revenue guarantees, keeping the project bankable without inflating tariffs to unacceptable levels.

Risks the private partner should own

Your firm has direct operational control over construction planning, procurement sourcing, and workforce deployment. This means construction completion risk, cost management, and defect liability belong on your side of the contract. Taking these risks is how private firms earn their return; accepting them is also what justifies the premium over a traditional engineering, procurement, and construction contract.

Operational efficiency risk during the concession period sits with you as well. Maintenance standards, staffing decisions, and service delivery quality are within your control, so the financial consequences of performing below the contracted service level should stay on your balance sheet. What you should push back on is when authorities attempt to bundle in risks like competing infrastructure development or force majeure events without adequate compensation provisions.

Risks that should be shared

Some exposures genuinely sit at the boundary between public and private control, and forcing them entirely onto one party creates unnecessary project stress. Exchange rate risk on foreign-denominated debt, archaeological discovery delays, and geotechnical surprises that standard investigation methods would not detect are common examples. These are best handled through shared responsibility clauses, such as cost-sharing thresholds or defined compensation events that trigger a process rather than automatic liability.

How to build a risk allocation matrix

A risk allocation matrix is the practical tool that converts abstract risk principles into a structured, document-level record of who owns what during a PPP concession. Building one before you finalize your bid position forces your team to make explicit decisions rather than leave exposure ambiguous. For any firm serious about risk allocation in PPP projects, the matrix is not a compliance artifact; it is a working document that shapes your bid price, your financing conversations, and your contract negotiation strategy.

Start with a complete risk inventory

Your matrix is only as useful as the risk list it covers. Before you assign ownership to anything, pull every risk event mentioned in the concession document, the draft agreement, and the project information memorandum. Group them into the core categories you already know: construction and completion, demand and revenue, political and regulatory, force majeure, and operational performance. Do not rely on memory or a generic template, because state-level concession documents in India regularly introduce sector-specific risks that standard frameworks miss, such as water table variability in irrigation PPPs or passenger ramp-up periods in metro contracts.

- List the risk event in plain language

- Record the relevant clause or document reference

- Note whether the contract assigns the risk explicitly or leaves it ambiguous

Score each risk by probability and impact

Once you have the full inventory, score each risk on two dimensions: likelihood of occurrence and financial impact if it materializes. Use a simple scale, such as low, medium, and high, applied consistently across all line items. This step tells you where to concentrate your analysis time. A risk with low probability and low impact does not need the same scrutiny as one with medium probability and catastrophic financial impact, such as a land acquisition delay on a project with a fixed concession start date.

The risks that sink PPP projects are almost never the ones bidders worried about; they are the medium-probability events that nobody priced because the contract document buried them in annexures.

Assign ownership and document the rationale

After scoring, assign each risk to the public authority, the concessionaire, or a shared category with a defined cost-sharing threshold. Write a one-line rationale for every assignment so your legal and finance teams can defend the logic during lender due diligence. Lenders scrutinize the matrix during financial close, and unexplained ownership decisions create negotiation delays that push your project timeline back by months.

How risk allocation affects bankability and pricing

Risk allocation in PPP projects does not stay inside the contract; it travels directly into your lender conversations and your bid model. The way risks are distributed across the concession agreement shapes whether a project can attract debt financing at a reasonable rate, and it sets the floor for how aggressively you can price your bid without destroying your returns. Understanding this connection lets you evaluate a tender's financial viability before you spend weeks building a detailed financial model.

How lenders read your risk matrix

Infrastructure lenders do not fund projects; they fund predictable cash flows backed by a contractual structure. When your debt advisory team takes a PPP project to a bank or institutional lender, the first thing credit committees examine is whether the risk allocation produces cash flows stable enough to service debt through a range of stress scenarios. If your concession agreement places demand risk entirely on you with no revenue floor, lenders apply a higher risk premium to the project's cost of debt, which increases your financing costs and reduces returns.

A risk matrix that transfers too many uncontrollable risks to the private partner does not make those risks disappear; it simply embeds them into a higher cost of capital that the public authority ultimately pays through inflated bid prices.

Lenders specifically look for the presence of termination payment provisions, change-in-law compensation clauses, and force majeure definitions with clear financial consequences. When these are absent or vaguely drafted, lenders either decline to fund the project or require equity sponsors to hold a larger buffer, which increases the equity component of your capital structure and pressures your internal rate of return.

How risk exposure flows into bid pricing

Your bid price is a direct expression of every risk you accept under the concession agreement. Construction risk exposure feeds into your contingency provision. Demand risk, when unhedged by guarantees, forces you to build a wider return cushion into your equity expectations. Regulatory and land acquisition uncertainty extends your project timeline assumptions, which increases financing costs and reduces net present value across the concession period.

Firms that price bids without a line-by-line risk review consistently underprice contingencies on the risks they accepted and overprice the risks they incorrectly assumed they could control. Running scenario analysis against your risk matrix before you finalize bid pricing is the discipline that separates competitive, fundable bids from those that either lose on price or win and then underperform.

Contract mechanisms that make allocation work

Defining who bears each risk in a concession agreement is only half the job. Contractual mechanisms are what give those allocations practical force, turning a risk matrix on paper into enforceable obligations that lenders, insurers, and both parties can rely on throughout the concession period. Without the right clauses in place, even well-structured risk allocation in PPP projects collapses under the weight of a single disputed event.

Termination payment provisions

Termination payments are the financial safety net that makes private investment in long-tenure PPPs possible. When a concession terminates early due to government default or force majeure, the concessionaire needs to know it will recover its outstanding debt and a defined portion of equity. Without a clear termination payment schedule in the contract, lenders treat the project as unbankable from the outset.

Your concession document should specify termination payment amounts for each trigger scenario separately:

- Government default termination: typically covers outstanding debt plus a defined percentage of equity

- Concessionaire default termination: usually limited to outstanding lender debt only

- Force majeure termination: a negotiated middle ground that protects lenders while limiting government exposure

Change-in-law and force majeure clauses

These two clauses protect the private partner from risk events that originate entirely outside its operational control. A change-in-law clause compensates you when new legislation or regulatory decisions materially alter the cost or revenue structure of your project. Force majeure provisions suspend your performance obligations and, in severe cases, trigger compensation or termination processes when extraordinary external events make delivery impossible.

Vague force majeure definitions are one of the most common drafting failures in state-level PPP documents across India, and they consistently produce disputes that delay projects by years.

Both clauses need precise, defined trigger events rather than broad language. Review the definitions carefully during your bid evaluation phase before committing resources.

Performance security and guarantee instruments

Performance securities, typically in the form of bank guarantees or letters of credit, protect the public authority when the concessionaire fails to meet construction milestones or service standards. For you as the private partner, the key concern is proportionality: guarantee amounts that exceed reasonable risk exposure tie up working capital and raise your financing costs without adding project value.

Structuring these instruments correctly, with clear release triggers tied to milestone completion, keeps your capital efficient while giving the contracting authority the assurance it needs to reach financial close.

Special considerations for PPPs in India

India's PPP landscape operates within a framework that differs in important ways from standard international models. Sector-specific policy shifts, multilayered procurement authorities, and a maturing but still inconsistent legal environment mean that firms practicing risk allocation in PPP projects here face challenges that generic frameworks do not fully address. Understanding these India-specific factors before you submit a bid can prevent costly surprises during execution.

The hybrid annuity model and its risk implications

The Hybrid Annuity Model (HAM) introduced by NHAI fundamentally changed how construction and demand risks split between public and private parties on national highway projects. Under HAM, the government pays 40% of the project cost during construction, and the concessionaire receives the remaining 60% through semi-annual annuity payments over the operations period. This structure removes demand risk from your balance sheet entirely, which lenders find far more comfortable than a pure toll model.

The trade-off is that your upfront capital requirement is significant, and any construction delay directly affects when annuity payments begin, making your schedule management critical to financial performance.

Your financial model under HAM needs to stress-test construction timeline slippage and its downstream effect on annuity receipt timing, because even a three-month delay compresses your returns across a 15-year concession period.

State-level procurement inconsistencies

Central government PPP documents, particularly those from NHAI and MoRTH, follow relatively standardized concession frameworks. State-level procurement is far more variable, with some states using outdated template agreements that lack adequate termination payment provisions, change-in-law clauses, or clear land acquisition responsibility timelines. When your firm evaluates a state highway, irrigation, or urban infrastructure PPP, you cannot assume that central-government-level protections apply.

Review each state concession document as a standalone instrument. Identify which risk categories the state template leaves ambiguous, because ambiguity at the contract stage becomes a dispute during operations.

Dispute resolution and arbitration frameworks

India's arbitration environment has improved significantly since amendments to the Arbitration and Conciliation Act, but enforcement timelines and institutional arbitration mechanisms still vary across states. Concession agreements that specify only domestic court jurisdiction without a defined arbitration pathway create significant uncertainty for your legal team and your lenders. Push for institutional arbitration clauses with defined timelines during contract negotiation, and flag any concession document that lacks a structured dispute resolution ladder before your firm commits to a bid.

Common mistakes and how to avoid them

Even firms with deep infrastructure experience make systematic errors when approaching risk allocation in PPP projects. These mistakes rarely happen because teams lack knowledge; they happen because bid timelines are compressed, concession documents are long, and the pressure to submit often overrides the discipline to review carefully. Knowing the most common failure patterns lets your team build checkpoints that prevent them before they cost you.

Accepting ambiguous risk language without flagging it

The most damaging clause in any concession document is often not the one that explicitly assigns you a risk, but the one that leaves ownership unclear. Ambiguous language around utility relocation timelines, site handover conditions, or environmental clearance responsibilities becomes a dispute the moment the ambiguity produces a financial consequence. At that point, the contracting authority and your firm will almost certainly interpret the clause in opposite directions.

Ambiguous risk clauses that both parties sign without resolution do not stay neutral; they become disputed liability the moment a project hits its first delay.

Review every clause where the document uses passive constructions or omits a responsible party entirely. Flag these during your bid evaluation phase and, where possible, seek written clarification from the authority before submission. If clarification is unavailable, price the ambiguity as if it falls entirely on you, because it very likely will.

Treating the risk matrix as a static document

Your risk matrix loses value the moment you stop updating it. Construction conditions change, regulatory environments shift, and what looked like a low-probability risk at bid stage can become an active issue within six months of project commencement. Firms that build a matrix during bid preparation and never revisit it lose the ability to respond to emerging exposures before they become unmanageable.

Schedule formal matrix reviews at each major project milestone, such as financial close, construction start, and first operational year. Assign a specific team member to own each update cycle so the review does not slip under workload pressure.

Underestimating state-level legal enforcement gaps

Central government concession frameworks come with established precedent and institutional support mechanisms. State-level agreements often do not, and enforcement of termination payment or change-in-law clauses can take years through the courts. Your legal review should verify whether the dispute resolution clause specifies institutional arbitration, because a generic "disputes shall be resolved by courts" provision creates timeline uncertainty that lenders will treat as a red flag during due diligence.

Next steps for your next PPP bid

Effective risk allocation in PPP projects does not happen during contract negotiations; it happens during bid evaluation, when your team still has time to walk away or reprice. Every principle covered in this article points toward one discipline: review concession documents for risk exposure before you commit bid resources, not after. Identify which risks the contracting authority has left ambiguous, stress-test your financial model against realistic downside scenarios, and build a risk matrix that travels with your project through every milestone review.

Your team does not need to do this manually. Arched reads concession documents automatically, flags unusual risk clauses, and surfaces qualification criteria so you can evaluate exposure in a fraction of the time. If your firm bids on infrastructure contracts and wants to stop missing critical clauses buried in annexures, explore what Arched can do for your pipeline before your next submission deadline.