Viability Gap Funding In PPP Projects: Limits & Eligibility

Understand the eligibility rules and limits for viability gap funding in ppp projects. Learn how to secure grants for Indian infrastructure development.

Some infrastructure projects make perfect sense on paper, strong public need, clear demand, but the financials just don't add up for a private developer. That's exactly the gap viability gap funding in PPP projects is designed to close. The Government of India's VGF scheme provides a capital grant of up to 20% of total project cost to make otherwise unviable public-private partnerships bankable, turning stalled proposals into funded, executable contracts.

For contractors and BD teams in the AEC space, understanding VGF isn't optional, it directly affects which projects hit the market, how they're structured, and what eligibility criteria you'll need to meet. Whether you're eyeing highway BOT contracts or urban infrastructure concessions, VGF-backed tenders carry specific qualification thresholds that can make or break your bid. At Arched, our platform parses these exact requirements from tender documents across 500+ government portals, helping firms identify VGF-linked opportunities they're actually positioned to win.

This guide breaks down the VGF scheme end to end: how the funding mechanism works, who qualifies, what the financial limits are, and how the approval process flows from proposal to disbursement. We've also included references to official government guidelines and practical context for firms building their PPP pipeline.

What viability gap funding means in PPPs

In a public-private partnership, the private party takes on the financial risk of building and operating infrastructure in exchange for future revenue, typically from user fees or availability payments. The problem is that many socially critical projects sit in low-income or underdeveloped areas where revenue projections don't justify the capital outlay. Viability gap funding in PPP projects is the government's mechanism to bridge that shortfall: a one-time capital grant that reduces the private partner's upfront investment burden enough to make the concession worth pursuing.

The core mechanics of a capital grant

VGF operates on a competitive bidding model. The government puts a project out for tender, and private developers bid on how little VGF they need to make the project viable. The lowest bidder, meaning the firm requesting the smallest grant, wins the concession. This keeps the public contribution efficient while ensuring private capital remains the dominant funding source in the project's financing structure.

The concession authority selects the bidder who requires the least government support, which directly ties public spending to market-tested project economics.

Once awarded, the grant disburses in phases, typically aligned with construction milestones rather than a lump-sum transfer. This structure ensures the government's money moves in step with actual project delivery, reducing the risk of funds being drawn without corresponding physical progress on site.

What counts as a PPP for VGF purposes

Not every arrangement between a government entity and a private firm qualifies, and you need to understand this distinction before assessing any opportunity. The project must involve private sector investment and risk-sharing under a formal concession agreement with a statutory authority. Your firm must also operate and maintain the asset for the full concession period, which means short-term construction-only contracts fall outside the scheme's scope entirely.

Why India uses viability gap funding for PPPs

India's infrastructure deficit is enormous, and the government cannot fund it alone. Public budgets cover only a fraction of what the country needs in roads, ports, urban transit, and water systems. Bringing private capital into these sectors makes practical sense, but private investors won't commit unless projected returns clear a minimum threshold. Viability gap funding in PPP projects exists specifically to hit that threshold without requiring full public financing.

VGF lets the government unlock private investment that would otherwise sit on the sidelines, multiplying the impact of every rupee of public spending.

The structural problem VGF solves

Many high-priority projects serve low-income populations or remote regions where toll revenues or user fees won't generate the returns a private developer needs. Without intervention, these projects simply don't get built. VGF fills the gap by reducing the equity burden on the private partner just enough to make the numbers work, while keeping the government's contribution capped and competitive.

Alignment with national infrastructure goals

India's National Infrastructure Pipeline targets trillions in investment across sectors. Private participation is essential to meet those targets, and VGF is one of the primary tools the Department of Economic Affairs uses to activate that participation at scale.

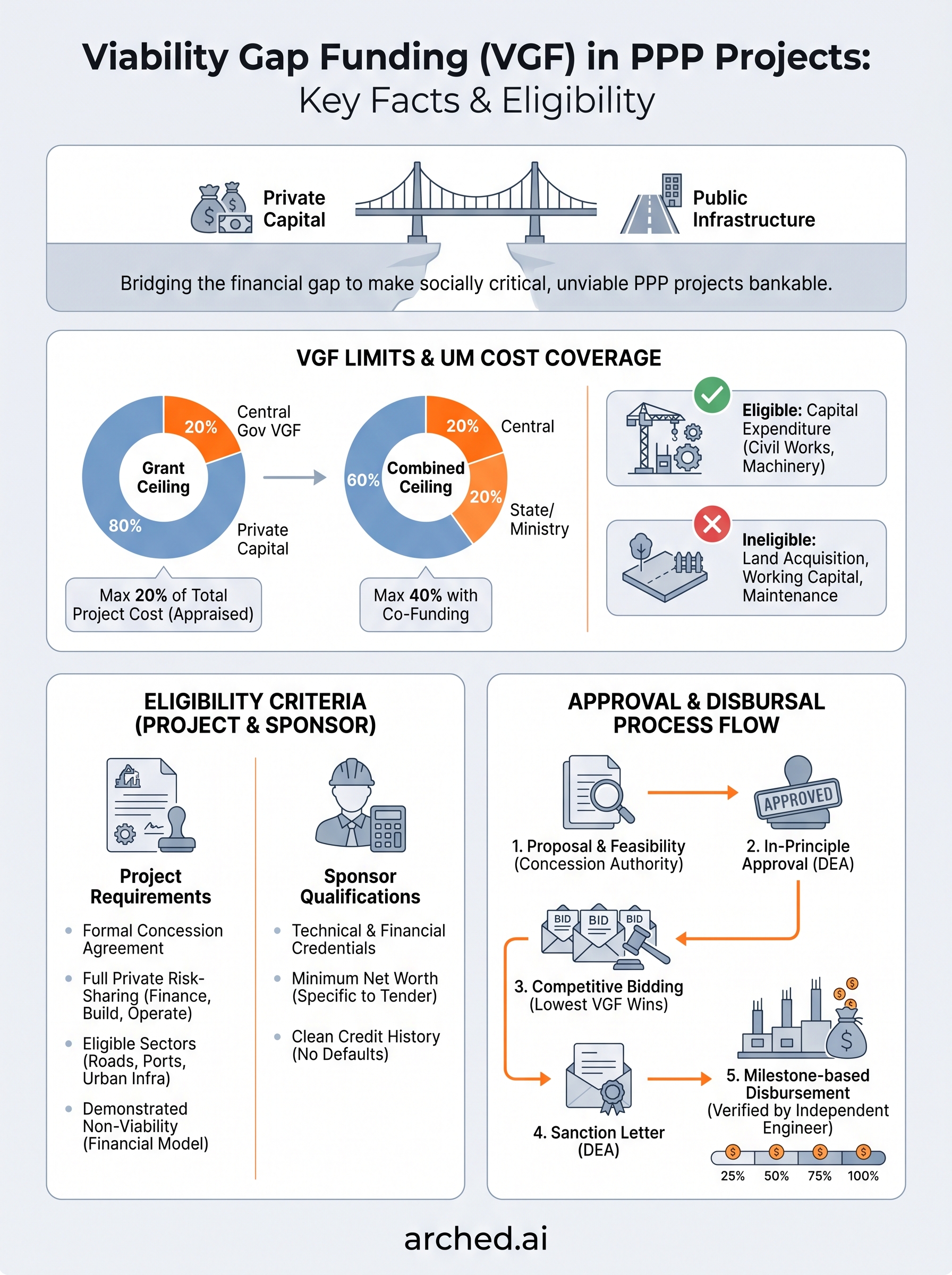

Eligibility for VGF in Indian PPP projects

Before you assess any viability gap funding in PPP projects opportunity, you need to confirm both the project and your firm meet the scheme's baseline requirements. The Department of Economic Affairs sets these criteria under the VGF scheme guidelines, and the concession authority checks them during the bid evaluation stage.

Project-level requirements

The project itself must clear several conditions before it qualifies for VGF consideration. Your target opportunity must tick all of these boxes:

- The project must be implemented through a formal concession agreement with a government or statutory authority

- It must involve private sector financing, construction, and operation for the full concession term

- The sector must fall within eligible categories, including roads, railways, ports, airports, urban infrastructure, and power

- The project must demonstrate commercial non-viability without the grant, supported by a detailed financial model

Sponsor qualifications

Your firm must hold the technical and financial credentials that the concession authority specifies in the RFP. This typically includes a minimum net worth, relevant project experience in the sector, and a clean credit history with no loan defaults.

Meeting the project eligibility threshold is necessary, but your firm's own qualification criteria are what determine whether you can actually submit a compliant bid.

VGF limits and what costs it can cover

The Department of Economic Affairs caps viability gap funding in PPP projects at 20% of the total project cost. If the sponsoring ministry or state government co-funds the gap, the combined ceiling rises to 40%, with each party contributing up to 20%. Your bid strategy needs to account for these hard limits from the start.

If your project's funding gap exceeds 40% of total project cost, VGF alone cannot make it bankable, and you'll need to revisit the concession structure entirely.

The 20% cap and how it's calculated

The grant ceiling applies to the total project cost as appraised by the lead financial institution, not your internal estimate. This distinction matters because the appraised figure sets the absolute upper bound on what the government will contribute.

Any cost overruns beyond the appraised amount fall entirely on your firm. Your financial model and bid pricing must absorb that risk before you submit.

Eligible and ineligible cost components

VGF covers capital expenditure only, so civil works, equipment, and construction-related costs qualify. Land acquisition is typically excluded from the appraised total for calculation purposes. Check each project's concession agreement to confirm, because ineligible cost items reduce the effective grant available to your firm.

- Civil works and construction: eligible

- Plant and machinery: eligible

- Land acquisition: not eligible

- Working capital or maintenance reserves: not eligible

How the VGF approval and disbursal process works

The approval process for viability gap funding in PPP projects runs through the Department of Economic Affairs (DEA) and involves multiple layers of review before a single rupee moves. Your concession authority, whether a central ministry or a state government body, submits the project proposal to the DEA along with a detailed financial model and feasibility report. The DEA then appraises the proposal, often with input from the lead financial institution, before granting in-principle approval.

Getting in-principle approval early is critical because it signals market credibility to lenders and co-investors who are evaluating your project's financing structure.

From proposal to sanction

Once the DEA grants in-principle approval, the competitive bidding process opens and shortlisted developers submit their VGF bids. The concession authority evaluates bids on the lowest-grant basis and issues a formal sanction letter to the selected developer, confirming the maximum grant amount the project will receive.

Disbursement tied to milestones

Your grant does not arrive as a lump sum. The DEA releases funds in tranches aligned to verified construction milestones, confirmed by an independent engineer appointed under the concession agreement. Each tranche requires documented proof of physical progress before the next disbursement triggers.

Key takeaways and next steps

Viability gap funding in PPP projects works as a targeted capital grant, capped at 20% of appraised project cost, to make commercially unviable but socially necessary infrastructure bankable. The scheme runs on a lowest-bid-wins model, which means your bid strategy directly determines how much public support you draw and whether you win the concession. Projects must fall within eligible sectors, involve full private risk-sharing, and demonstrate a verified funding gap before the DEA considers them.

Your firm's qualification credentials matter as much as the project's eligibility. Technical experience, net worth thresholds, and a clean credit history are the levers that determine whether you can submit a compliant bid in the first place. Disbursement ties to construction milestones, so your cash flow planning must account for phased grant releases rather than upfront capital. To find VGF-linked tenders matched to your firm's actual credentials, explore what Arched's platform can do for your pipeline.