EPC Vs HAM Vs BOT Vs TOT: Key Differences In Highway PPPs

Compare EPC vs HAM vs BOT vs TOT to understand risk and funding in Indian highway PPPs. Learn how to choose the right model for your firm’s bidding strategy.

Every highway contract awarded in India carries a specific risk-sharing structure baked into its model, and if your BD team doesn't understand how EPC vs HAM vs BOT vs TOT works, you're either bidding blind or walking past contracts you could win.

These four models govern how highway projects are funded, built, and operated under Public-Private Partnerships (PPPs). Each one distributes financial risk, revenue rights, and construction responsibility differently between the government and the private contractor. For infrastructure firms chasing NHAI and state highway tenders, knowing which model applies to a project isn't academic, it directly affects your capital exposure, eligibility requirements, and long-term revenue potential. It's also the kind of detail that gets buried inside lengthy tender documents, which is exactly why we built Arched to parse and surface these distinctions automatically.

This article breaks down all four models, their mechanics, risk structures, and real-world applications, so you can evaluate opportunities with precision rather than guesswork. Whether you're an EPC contractor weighing a shift toward HAM projects or a concessionaire exploring TOT assets, the comparison ahead will give you the clarity to make that call.

Why highway PPP models matter in India

India's road sector generates hundreds of active tenders at any given time, and each one gets structured under a specific contract model before it reaches a procurement portal. These models aren't just legal categories printed in a document header. They determine how financial risk moves between the government and the private sector, how long your revenue exposure lasts, and what financing strength your firm needs to demonstrate just to qualify for a bid. Treating contract models as background detail rather than core bid intelligence puts your team at a real disadvantage before the evaluation even starts.

The scale of India's highway investment

NHAI and state highway authorities together represent one of the most active infrastructure procurement markets in the world. India's Bharatmala Pariyojana program set a target to build and upgrade over 50,000 kilometers of national highways with a total outlay exceeding Rs 10 lakh crore. That volume means the model attached to any single project carries direct financial consequences for every firm competing in this space.

The government doesn't apply a single model across all projects. It selects contracting structures based on traffic certainty, project complexity, and how much private capital the market can realistically absorb at a given point. A toll corridor near a major metro reads very differently to a financier than a greenfield stretch through a low-density rural district. The model chosen for each project reflects that underlying economic reality.

How model selection shapes your bid position

When you evaluate epc vs ham vs bot vs tot opportunities in your pipeline, the model classification directly sets your capital requirement, defines your cash flow timeline, and determines whether your firm's balance sheet qualifies at all. An EPC contractor working on government-funded construction faces a fundamentally different risk profile than a concessionaire acquiring a TOT bundle on an existing toll corridor with five years of traffic data behind it.

Getting the model wrong at the bid evaluation stage can cost your team months of work chasing a contract your firm was never structured to win.

Why policy shifts create bidding windows

India's central government has rotated its preferred model more than once based on market stress and private sector appetite. BOT dominated through the mid-2000s, then stalled projects in the early 2010s pushed NHAI toward EPC. HAM arrived in 2016 as a deliberate middle path to bring private co-investment back without forcing concessionaires to absorb full traffic risk.

Recognizing these shifts helps you spot emerging tender clusters before competitors do, because policy pivots typically flow through project pipelines six to eighteen months before they show up as awarded contracts in the public record.

How EPC, BOT, HAM, and TOT work in practice

Understanding epc vs ham vs bot vs tot becomes much clearer once you see each model as a specific deal structure rather than a label. The government chooses a model based on who carries the financial load and how revenue from the road gets distributed once it's built.

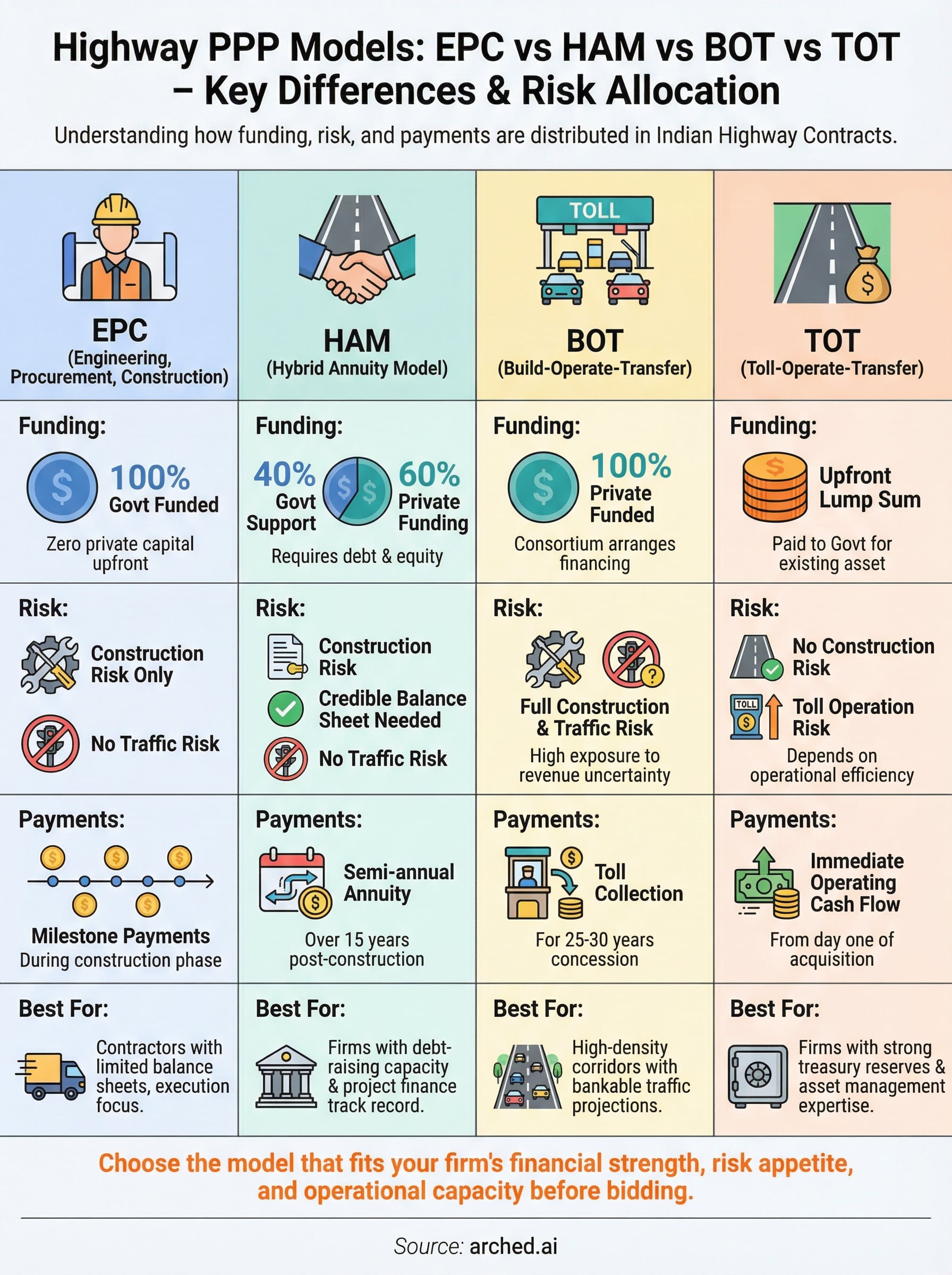

EPC and BOT: The original two poles

In an EPC contract, the government funds 100% of construction. You win the project, deliver the road within scope and schedule, collect your progress-linked payments, and walk away with no long-term revenue stake. Your risk is execution risk: cost overruns and delays. The National Highways Authority of India uses EPC heavily for stretches where toll viability is uncertain or where private financing appetite is low.

BOT flips that structure entirely. You arrange private financing, build the corridor, and operate the toll plaza for a concession period, typically 25 to 30 years, recovering your investment through toll collections. Traffic shortfall is your problem. BOT only makes sense on high-density corridors where traffic projections are bankable, which is why lenders scrutinize feasibility reports so closely before committing debt to a BOT project.

HAM and TOT: The newer hybrid models

HAM splits the funding between the government and the private developer, with NHAI contributing 40% of the project cost as construction support and the balance raised by you. Once construction is complete, the government pays you a semi-annual annuity over 15 years. You avoid full traffic risk, but you still need a credible balance sheet and debt-raising capacity to qualify.

TOT is structurally different from the other three because you're not building anything. You acquire the right to collect tolls on an already operational highway bundle, paying an upfront lump sum to NHAI for the concession.

TOT suits firms with strong financial reserves and asset management expertise, since your return depends entirely on optimizing toll operations and keeping maintenance costs in check over the concession term.

Key differences across funding, risk, and payments

When you compare epc vs ham vs bot vs tot side by side, the clearest lens is to track three variables: who puts in the construction capital, who absorbs revenue uncertainty, and when cash actually flows back to your firm. Those three factors determine whether a contract fits your current financial position before you spend a rupee on bid preparation.

Funding structure and government contribution

The funding split sets the entry barrier for each model. EPC requires zero private capital upfront since the government covers the entire project cost, making it accessible to contractors with limited balance sheets. HAM requires you to arrange roughly 60% of project funding through debt and equity, with NHAI covering the remainder as construction support. BOT places the full financing burden on your consortium, while TOT demands a single large upfront concession fee paid to NHAI before operations begin.

| Model | Government Funding | Private Funding |

|---|---|---|

| EPC | 100% | 0% |

| HAM | 40% | 60% |

| BOT | 0% | 100% |

| TOT | 0% (receives fee) | Upfront lump sum |

Risk allocation across traffic and construction

EPC limits your exposure to construction and execution risk only. BOT stacks both construction risk and full traffic revenue risk on your consortium for the entire 25 to 30-year concession period, which lenders examine carefully before committing debt.

Your risk profile should match your firm's capital structure before you commit to any of these models, not after you submit the bid.

HAM removes traffic risk but keeps construction risk with you. TOT eliminates construction risk entirely since the road already exists, but your returns depend entirely on toll collection performance and disciplined maintenance cost management.

Payment timing and cash flow

EPC delivers milestone-based progress payments during construction, giving you predictable short-term income. HAM shifts to semi-annual government annuity payments post-construction across 15 years, which suits firms comfortable with deferred but guaranteed revenue streams.

BOT generates toll income from day one of operations but only after a long construction phase with no revenue. TOT produces immediate operating cash flow from an existing toll asset the moment you complete the acquisition.

When to choose each model for a highway project

Selecting the right model from epc vs ham vs bot vs tot starts with an honest assessment of your firm's current financial position and operational capacity. No single model fits every firm at every stage of growth, so matching your balance sheet strength to the contract structure before you invest time in bid preparation saves you from expensive dead ends.

Matching your capital position to the model

EPC suits firms that generate steady revenue from construction execution but lack the balance sheet to raise project-level debt or absorb multi-year revenue uncertainty. If your firm is growing its NHAI project count without stretching into concession financing, EPC contracts give you volume without forcing a capital structure you're not ready for. HAM is the right step up when you've built credible relationships with project finance lenders and can demonstrate a track record of on-time delivery, since annuity payments reward execution discipline over traffic speculation.

BOT is only the right call when your consortium has independently verified traffic projections and a lender group already aligned on debt structure before the bid goes in.

Matching the corridor profile to your strategy

TOT works when your firm carries strong treasury reserves and asset management capability, because you're acquiring operational toll corridors rather than winning construction work. The upside comes from operational efficiency gains over the concession term, not from building something new. BOT fits greenfield corridors in dense economic zones where traffic forecasts carry genuine confidence and your consortium can sustain the financing structure across a 25 to 30-year concession.

HAM fills the middle ground: use it when a corridor has moderate traffic uncertainty and NHAI is co-funding construction, giving you a defined annuity return without betting your firm on toll revenue projections you can't fully control.

Common tender pitfalls and how to spot them early

Bid teams regularly lose time and money on contracts that were never a realistic fit, and most of those losses trace back to mistakes made in the first 30 minutes of document review. When you're scanning epc vs ham vs bot vs tot opportunities across multiple portals simultaneously, the volume pressure pushes teams toward shortcuts that create expensive problems later.

Misreading the model classification

The contract model is almost never labeled cleanly on the portal listing. It sits inside the Request for Proposal or the concession agreement draft, sometimes buried three documents deep. Bid managers who rely on portal summaries or keyword filters frequently misclassify HAM projects as BOT, which means their capital adequacy calculations are wrong before anyone opens a spreadsheet.

Pulling the full tender package before your team commits any evaluation time is the single most reliable way to avoid misclassifying a project at the start.

Check the payment mechanism clause and the risk allocation schedule in the first read-through. If annuity payments appear alongside a government contribution percentage, you're looking at HAM. If toll rights are assigned to your consortium for a 25-plus year concession with no construction support, that's BOT.

Missing qualification criteria buried in annexures

Many firms discover disqualifying criteria only after they've invested days in bid preparation. Net worth thresholds, minimum annual turnover requirements, and specific project experience mandates often appear in annexures rather than the main eligibility section, and portal previews rarely surface them.

Build a document checklist that forces your team to read every annexure and technical specification sheet before marking a tender as viable. Look specifically for experience requirements tied to project size bands, since NHAI often sets thresholds that exclude firms whose largest completed project falls below the required benchmark value by even a small margin.

Final takeaways

The epc vs ham vs bot vs tot comparison isn't a theoretical exercise. Every contract model carries a specific set of financial obligations, risk exposures, and qualification requirements that either fit your firm's current position or they don't. EPC suits execution-focused contractors who want predictable milestone payments without long-term revenue bets. HAM works when you can raise project-level debt and want a government-backed annuity return. BOT demands a high-traffic corridor and a lender-aligned consortium before you commit. TOT requires treasury strength and operational discipline on existing assets.

Most bid losses in this space trace back to misreading the model early, missing buried qualification criteria, or chasing contracts that don't match your balance sheet. Your team can cut that risk significantly by getting the full document package reviewed before any bid commitment. If you want to reduce that manual workload and surface the right opportunities faster, explore what Arched does for BD teams.