Unconditional Bank Guarantee Meaning: On-Demand BG Explained

Master the unconditional bank guarantee meaning for Indian govt tenders. Learn how on-demand BGs work, differ from LCs, and how to manage your project risk.

Every government tender in India worth its salt demands a bank guarantee, usually an Earnest Money Deposit (EMD) or a Performance Bank Guarantee (PBG). And buried in the tender documents, you'll often find a specific requirement: the guarantee must be unconditional and irrevocable. Miss that detail, and your bid gets disqualified before anyone even reads your technical proposal. Understanding the unconditional bank guarantee meaning is not optional for firms bidding on public infrastructure contracts; it's foundational.

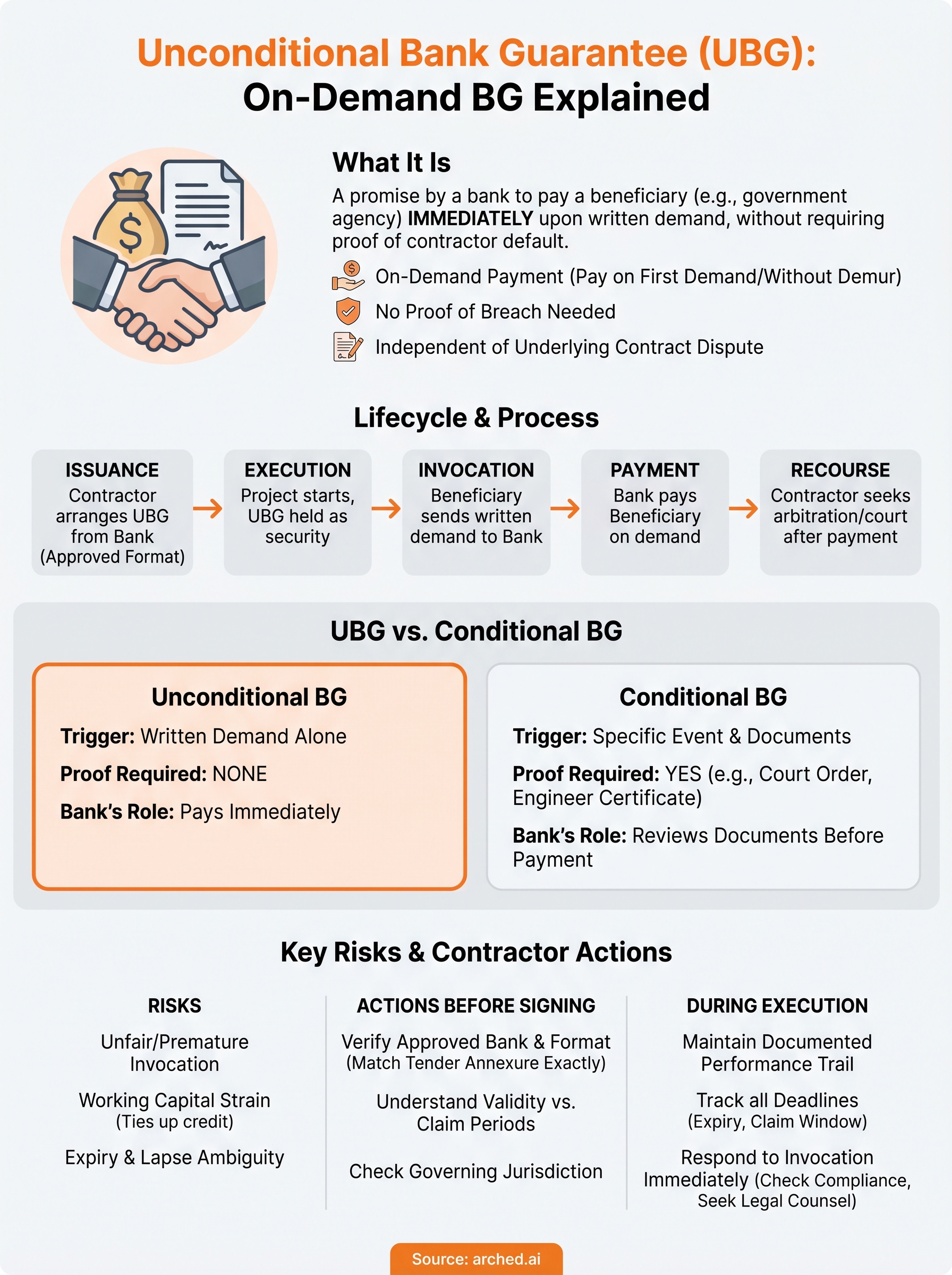

An unconditional bank guarantee, also called an on-demand bank guarantee, obligates the issuing bank to pay the beneficiary (typically the government agency) the moment a demand is made, without requiring proof that the contractor actually defaulted. That's a significant financial exposure. It shifts risk squarely onto the contractor and the bank, and it operates very differently from a conditional guarantee, where the beneficiary must first prove a breach before collecting.

This distinction matters enormously for infrastructure firms, consultancies, and contractors navigating high-value bids on platforms like GeM, CPPP, and state e-procurement portals. At Arched, our platform parses tender documents to flag exactly these kinds of clauses, BG requirements, unusual risk terms, qualification criteria, so your BD team doesn't have to read 80-page PDFs line by line. But understanding what those flagged clauses actually mean? That's where this guide comes in.

This article breaks down the legal structure of unconditional bank guarantees, how Indian courts have interpreted them, the key differences from conditional guarantees, and what contractors should watch for before committing to one.

Why unconditional bank guarantees matter in India

India's public procurement market is enormous. The government spends roughly 15-20% of GDP on public contracts every year, covering roads, bridges, metro systems, irrigation networks, urban infrastructure, and defense installations. For firms in the Architecture, Engineering, and Construction (AEC) sector, government contracts often represent the primary revenue pipeline. Almost every one of those contracts requires some form of bank guarantee, and the vast majority of them specifically demand an unconditional variant.

The scale and structure of Indian public procurement

The sheer volume of tenders across platforms like GeM, CPPP, and IREPS, plus hundreds of state-level e-procurement portals, means that bank guarantees are not occasional paperwork. They are a constant operational reality. At any given time, a mid-sized infrastructure firm might have multiple BGs outstanding simultaneously, each tying up working capital and carrying the risk of sudden invocation by a government agency.

Grasping the unconditional bank guarantee meaning is therefore not just a legal exercise. It directly shapes how your firm manages cash flow, credit limits, and risk exposure across your entire project portfolio. A single invoked BG on a large contract can wipe out the operating margin from several smaller projects.

An unconditional bank guarantee puts the payment obligation entirely on the bank, with no ability for the contractor to delay or dispute payment once a demand is made.

How Indian courts interpret unconditional BGs

Indian courts have consistently and firmly upheld the on-demand nature of unconditional bank guarantees. The Supreme Court of India, in a line of judgments starting with U.P. Co-operative Federation Ltd. v. Singh Consultants and Engineers (1988), established a clear principle: courts will not ordinarily interfere with the encashment of an unconditional bank guarantee, except in cases of clear fraud or irretrievable injustice.

This legal position has been reinforced repeatedly in subsequent rulings. The court's reasoning is straightforward: bank guarantees are independent of the underlying contract. The dispute between the contractor and the employer over whether a default actually occurred is treated as a separate matter entirely. The bank pays first; the contractor litigates later. This approach protects the commercial reliability of BGs as financial instruments, but it places enormous pressure on you as the contractor to ensure performance obligations are met before a guarantee even risks being called.

Why government agencies prefer unconditional BGs

From the government's perspective, the preference for unconditional guarantees is rational and deliberate. Public agencies managing infrastructure procurement at scale cannot afford to enter legal proceedings every time a contractor disputes a performance failure. An unconditional BG gives them immediate access to funds to cover project delays, incomplete work, or contractual shortfalls, without waiting for arbitration or court orders to conclude.

This preference is now institutionalized across procurement frameworks. The General Financial Rules (GFR) 2017, which govern central government procurement in India, and state-level procurement manuals all specify that performance guarantees must be unconditional and irrevocable. When you submit a bid on a central or state government tender, the BG format is usually prescribed in the tender documents, and deviating from that format, such as submitting a conditional BG, is grounds for immediate rejection.

The practical implication for your firm is clear: you do not negotiate whether to provide an unconditional BG on most Indian government contracts. You accept the format, or you don't bid. What you can and must do is understand exactly what you're committing to, verify the BG clause language against the prescribed format, and manage your project execution in a way that keeps invocation off the table entirely.

What makes a bank guarantee unconditional

A bank guarantee earns the label "unconditional" based on a single defining characteristic: the issuing bank must pay the beneficiary upon receiving a written demand, with no right to require evidence of the contractor's fault. The beneficiary does not need to prove a breach, demonstrate losses, or attach documents showing a default occurred. The demand alone triggers the payment obligation, and that simplicity is precisely what gives unconditional BGs their commercial power and legal weight in Indian public procurement.

The "pay on first demand" clause

The core element you will find in every unconditional BG is the "pay on first demand" clause, sometimes written as "pay on demand" or "without demur." This language is the mechanical heart of the instrument. When the beneficiary issues a written demand, the bank must process the payment within the period specified in the guarantee itself, without pausing to verify whether the underlying contract dispute has any merit.

The phrase "without demur, merely on demand" in a BG document is the clearest signal that the instrument is unconditional and will be honored regardless of any contractor objection.

This is where grasping the unconditional bank guarantee meaning becomes operationally critical for your firm. Contractors sometimes assume they can instruct their bank to hold payment while a dispute is ongoing. That assumption is wrong. Once the BG is unconditional, the bank's obligation runs to the beneficiary alone, not to the contractor who arranged the guarantee. Your bank cannot legally stall on the basis of your instructions once a compliant demand arrives.

The independence principle and what it means for you

An unconditional BG draws its legal strength from what courts call the independence principle: the guarantee is legally separate from the contract that created it. Even if your firm has a valid counterclaim against the government agency, such as delayed site handover or client-driven scope changes, that dispute has no bearing on the bank's obligation to pay when a compliant written demand arrives.

Because of this separation, the language in your BG document must be read entirely in isolation from the rest of the tender contract. Your firm's legal remedies lie in arbitration or court after payment has been made, not before. That sequencing is standard across Indian public procurement, and you need to factor it into risk planning from the moment you decide to bid. The following phrases in a BG document each signal unconditional status:

- "Without demur": payment without objection or hesitation

- "Without reference to the contractor": bank acts independently

- "On first written demand": a single demand triggers full liability

- "Notwithstanding any dispute": underlying contract disputes are irrelevant to payment

How an on-demand BG works step by step

Understanding the unconditional bank guarantee meaning becomes more tangible when you trace the actual lifecycle of the instrument from issuance to potential invocation. The process follows a fixed sequence of events, and knowing each stage helps your firm identify where the real risks sit and what actions you can actually control.

Step 1: Issuance and submission

Your firm approaches its bank or financial institution to arrange the guarantee before or alongside bid submission. The bank issues the BG document using the format prescribed in the tender, which already contains the unconditional, irrevocable, and on-demand language. You then submit this document to the government agency as part of your bid or contract execution package. The agency verifies the BG format, checks that the issuing bank appears on the approved list, and confirms the validity period covers the required duration.

Step 2: The project execution phase

Once the contract begins, the BG runs in the background as a standing obligation. The government agency holds it as security throughout the project. Your obligation during this phase is straightforward: perform as per contract terms to keep the guarantee from being called. If you meet milestones, submit compliant deliverables, and adhere to quality standards, the BG will never be invoked. Firms with strong project delivery rarely see their BGs touched.

The safest way to manage an unconditional BG is to treat it as the cost of a default you intend never to trigger, while building the execution discipline that keeps invocation off the table entirely.

Step 3: Invocation by the beneficiary

If the agency decides to invoke the guarantee, it sends a written demand letter to the issuing bank stating that payment is required under the BG. Critically, the agency does not need to explain why or provide evidence of your default. The bank receives this demand, checks that it is formally compliant with the BG terms (correct reference number, within validity period, signed by authorized signatory), and processes payment. Your objection to the invocation, however legitimate, does not stop this process.

Step 4: Recourse after payment

After the bank pays, it will debit your account or call in collateral you provided when arranging the BG. At that point, your only formal remedy is to pursue the government agency through arbitration or litigation, claiming that the invocation was fraudulent or that you are owed compensation for the amounts paid. Courts will not reverse a completed payment except in proven fraud cases. Getting the contract execution right the first time is far more valuable than any legal strategy you can build after a demand has already been honored.

Unconditional BG vs conditional BG

The difference between an unconditional and a conditional bank guarantee comes down to one central question: what does the beneficiary need to show before the bank pays? Understanding the unconditional bank guarantee meaning already gives you half the answer. With an unconditional BG, the beneficiary submits a written demand and the bank pays, full stop. With a conditional BG, the beneficiary must first satisfy specific documentary or evidentiary requirements before the bank releases any funds. That structural difference carries major consequences for how risk is allocated between the parties.

What a conditional BG requires from the beneficiary

A conditional BG ties the bank's payment obligation to proof of a specific triggering event. The beneficiary cannot simply send a demand letter. They must attach supporting documents, such as a court order, an arbitration award, a supervising engineer's certificate of non-performance, or a written confirmation of default from a named third party. Until the bank receives compliant documentation that matches the conditions written into the BG, it has no legal obligation to pay.

This requirement shifts meaningful protection back to you as the contractor. If your client makes an unfair or premature call on the guarantee, the bank functions as a gatekeeper, reviewing whether the submitted documents actually satisfy the stated conditions. You gain time to challenge the invocation through legal channels, negotiate a resolution, or demonstrate that the triggering event has not occurred. That buffer simply does not exist with an unconditional instrument.

In Indian government contracting, conditional BGs are almost never accepted because agencies managing large infrastructure procurement require immediate access to funds, and conditional instruments slow that process down significantly.

Why the distinction matters when you sign a contract

The practical gap between the two instruments is large enough that your legal and finance teams should treat them as entirely different products. A conditional BG resembles a performance bond in some respects: payment depends on establishing facts first. An unconditional BG is closer to a cash deposit held by the bank on the beneficiary's behalf, accessible on demand without friction or delay.

When you review a draft contract or tender document, check the BG format in the annexures carefully. Phrases like "on first demand," "without demur," or "notwithstanding any dispute" confirm that you are looking at an unconditional instrument, and you need to price the associated risk into your bid accordingly. If the format instead specifies documentary conditions, such as a default notice countersigned by a supervising engineer, the BG is conditional and carries a substantially different risk profile for your firm. Knowing which type you are committing to before signing protects your working capital and your legal position throughout the contract.

Unconditional BG vs letter of credit

Contractors and BD managers often conflate unconditional bank guarantees with letters of credit because both instruments involve a bank making a payment on behalf of a client. The underlying logic is actually quite different, and mixing them up in a contract negotiation or bid submission can create serious commercial problems. Grasping the unconditional bank guarantee meaning requires understanding not just what the instrument does, but what it is not, and a letter of credit is the most useful comparison to draw.

How the payment trigger differs

A letter of credit (LC) is primarily a trade finance instrument designed to facilitate a sale. The bank pays the beneficiary, typically a supplier or exporter, once that party presents specific documents proving that goods or services were delivered as agreed: a bill of lading, an invoice, an inspection certificate. The bank checks those documents against the LC terms before releasing funds. Payment follows proof of performance, which means the instrument rewards delivery.

An unconditional BG works in the opposite direction. It protects the beneficiary against non-performance or default by the contractor. The bank pays when the beneficiary submits a demand claiming that performance failed, without any documentary burden. No shipping documents, no inspection reports, no third-party certificates are required. The demand itself is enough.

The core distinction is directional: an LC pays when work is done, while an unconditional BG pays when work allegedly is not done.

| Feature | Unconditional BG | Letter of Credit |

|---|---|---|

| Primary purpose | Protects against non-performance | Facilitates payment for delivery |

| Payment trigger | Written demand alone | Compliant documents proving delivery |

| Documentary burden on beneficiary | None | Yes, specific documents required |

| Common use in Indian government contracts | Yes, mandatory | Rarely, mainly in trade contexts |

When to use each instrument

In Indian government contracting, you will almost never encounter an LC in place of a BG. Government agencies issue tenders that prescribe the BG format directly in the annexures, and that format is always unconditional and irrevocable. LCs appear in import-export transactions and supply chain financing, where one party needs assurance that payment will follow documented delivery.

Understanding when each instrument applies protects your firm from two separate mistakes. The first is submitting an LC-style conditional instrument in response to a government tender that demands an unconditional BG, which results in immediate bid disqualification. The second is accepting an unconditional BG from a subcontractor when a conditional instrument would give you better legal protection if a dispute over performance quality arises later in the project. Read the instrument type required, match it precisely, and verify that your bank issues the correct format before submission.

Where unconditional BGs show up in contracts and tenders

Knowing the unconditional bank guarantee meaning is only useful if you also know where these instruments appear in the contracts your firm actually signs. In Indian government contracting, unconditional BGs are not limited to one stage of the procurement cycle. They appear at multiple points across the bid and execution lifecycle, each carrying a different value, validity period, and set of conditions that your team must track simultaneously.

Earnest Money Deposits

An Earnest Money Deposit (EMD) is the first unconditional BG your firm typically encounters in any tender. The government agency requires it alongside your bid submission to confirm that you are serious about participating and will not withdraw your offer after the bid opening. EMD values are usually a fixed percentage of the estimated contract value, typically between 1% and 2%, and the BG must be valid well beyond the bid validity period to cover any re-bidding or evaluation delays. If you win the contract and then decline to sign, the agency invokes the EMD immediately, without any dispute process.

EMD bank guarantees are often the first test of whether your BG format matches the prescribed tender annexure exactly, and a format mismatch at this stage means outright disqualification.

Performance Bank Guarantees

Once you execute the contract, the Performance Bank Guarantee (PBG) replaces the EMD as the primary security instrument. PBG values are substantially higher, commonly 5% to 10% of the contract value, and the guarantee must remain valid through the defect liability period that extends beyond physical project completion. Agencies on platforms such as CPPP and state e-procurement portals prescribe specific PBG formats in the tender documents, and any deviation from those formats gives the agency grounds to treat the guarantee as non-compliant.

Advance Payment Guarantees

Many government contracts in the AEC sector offer a mobilization advance to help contractors fund early project expenses. Before disbursing that advance, the agency requires an Advance Payment Guarantee, which is also unconditional and irrevocable. The guarantee value reduces progressively as you recover the advance through running account bill deductions, but your bank must track those reductions carefully to ensure the outstanding BG liability matches the unrecovered advance at every stage.

Subcontract and JV Arrangements

Unconditional BGs also flow downstream within your supply chain. When your firm engages subcontractors on a government project, you will frequently demand performance security from them in the same unconditional format that the main client imposed on you. Similarly, in a joint venture structure, each partner may be required to furnish a BG to the lead partner or directly to the client, depending on the JV agreement's terms. Your finance team needs a consolidated view of all outstanding BG obligations across the full project structure to manage credit limits effectively.

Key clauses to read before you sign or accept a BG

Before your firm commits to an unconditional bank guarantee, whether you are the contractor furnishing one or the agency receiving one, clause-level review is non-negotiable. Most BG disputes in Indian infrastructure contracting do not arise from bad faith. They arise because one party misread the validity date, missed a notice requirement, or assumed the issuing bank's approved status without confirming it. Taking 30 minutes to check the right clauses before signing saves significant legal cost and working capital later.

Validity Period and Claim Deadline

The validity clause tells you two things: when the guarantee expires and how long after expiry the beneficiary can still submit a written demand. These are often different dates, and conflating them is a common and expensive mistake. Many BG formats include a claim period of 30 to 60 days beyond the stated validity end date, which means the agency can invoke the guarantee even after the project is closed out if they act within that window. Verify both dates explicitly and ensure your bank flags the claim deadline in its internal tracking system, not just the nominal expiry date.

Treat the claim deadline as the true end date of your BG liability, not the validity date printed at the top of the document.

Approved Bank and Format Compliance

Government agencies maintain lists of approved banks from which they accept guarantees. State procurement portals and central agencies like CPWD and NHAI publish these lists in their tender documents or on their procurement websites. If your issuing bank does not appear on that approved list, the agency can reject the BG entirely, even if the document language is otherwise perfect. Separately, check that every word in the BG format matches the prescribed annexure in the tender. Agencies can and do reject guarantees that substitute phrases or add qualifications not present in the approved template.

Governing Jurisdiction

The jurisdiction clause specifies which court or arbitral authority handles disputes arising from the guarantee itself, separate from the underlying contract. In some BG documents, this clause is left blank or defaults to the bank's registered city rather than the project location. That detail matters if the agency invokes the guarantee and you need to seek urgent interim relief from a court. A jurisdiction clause that places proceedings in a city where neither your firm nor the project site is located adds cost and delays to any legal response you need to mount quickly.

Fully understanding the unconditional bank guarantee meaning means reading these clauses before your signature goes on the document, not after a demand letter arrives at your bank's counter.

Risks for contractors and how to reduce them

Committing to an unconditional bank guarantee exposes your firm to financial risk the moment the document is signed, not only when a dispute arises. The unconditional bank guarantee meaning is inseparable from the risk it carries: the bank pays the beneficiary on demand, and your firm absorbs the consequences. Recognizing the specific risk categories that contractors face, and acting on them before a problem develops, is the most practical way to protect your margins and your credit lines.

Unfair or Premature Invocation

Government agencies sometimes invoke a BG before a dispute is fully developed or before your firm has had a reasonable opportunity to remedy a performance issue. Because the bank has no legal duty to verify the merits of the demand, payment goes through regardless of whether the invocation is justified. Indian courts will intervene only in cases of clear and established fraud, a bar that is deliberately high and rarely met in practice.

Your best protection against premature invocation is a documented paper trail showing timely performance, because courts assess fraud claims against evidence, not intentions.

Your team should maintain contemporaneous records of every milestone completion, site inspection, and client communication throughout the project lifecycle. If an agency raises a concern, respond in writing immediately and acknowledge receipt. That documentation becomes your evidence base if you pursue arbitration after an unjust invocation.

Working Capital Strain

Every unconditional BG your firm issues ties up bank credit limits and cash collateral for the duration of the guarantee's validity period, which often extends well beyond practical project completion. For firms running multiple government contracts simultaneously, the aggregate BG exposure can consume a significant portion of available credit, limiting your ability to bid on new work or fund ongoing operations.

Reduce this strain by negotiating realistic validity periods at the contract stage rather than accepting whatever the draft tender specifies. Many agencies set validity periods far longer than necessary for the actual risk window, and a targeted discussion during pre-bid clarification meetings can sometimes result in a shortened period without affecting your eligibility.

Expiry and Lapse Risks

A BG that lapses before the agency formally returns it leaves your firm in an ambiguous position. Agencies may claim the right to invoke during a claim period that extends beyond the nominal expiry date, as discussed earlier in this article.

Build a centralized BG tracking system that flags the following deadlines well in advance:

- Nominal validity expiry date

- Claim window end date (typically 30 to 60 days after expiry)

- Extension request deadline if the project timeline shifts

- Scheduled return date from the agency after project closeout

How to issue, invoke, and respond to invocation

The practical side of the unconditional bank guarantee meaning comes into focus when you work through three distinct actions: issuing a BG, invoking one as a beneficiary, and responding when your own BG gets called. Each stage has its own process, and a mistake at any of them carries direct financial consequences for your firm.

Issuing a BG correctly

When your firm needs to furnish an unconditional BG, start by confirming that your bank appears on the agency's approved list of issuing banks, which is usually published in the tender annexures or on the procurement portal. Once confirmed, submit the tender's prescribed BG format to your bank exactly as written. Do not allow your bank to add standard internal qualifications or modify the "pay on first demand" or "without demur" language, because any deviation from the prescribed format gives the agency grounds to reject the instrument outright.

Your bank will require collateral or a cash margin, typically between 10% and 25% of the BG value, before issuing the document. Factor this into your working capital planning before you submit a bid, because multiple simultaneous BGs can absorb a significant portion of your available credit limits quickly.

Invoking a BG as the beneficiary

If you are the agency or the party holding a BG and you need to invoke it, the process is straightforward. Send a written demand letter to the issuing bank citing the BG reference number, the amount being claimed, and the bank account details for remittance. The letter must be signed by an authorized signatory and submitted within the validity period, including any claim window specified in the document. You do not need to attach evidence of the contractor's default, because the unconditional nature of the instrument removes that requirement entirely.

Once a compliant written demand reaches the issuing bank, the payment process moves forward regardless of any objection from the contractor who arranged the guarantee.

Responding when your BG is invoked

When you receive notice that your BG has been invoked, act immediately on two fronts. First, contact your bank to confirm the demand is formally compliant with the BG terms, specifically that the reference number, validity period, and authorized signature are all in order. A non-compliant demand gives the bank grounds to reject it, which buys you time. Second, engage legal counsel the same day to assess whether the invocation meets the narrow fraud threshold that Indian courts recognize as grounds for interim injunctive relief.

If the invocation is valid and the bank pays, document every project record, correspondence, and milestone certificate you hold, because that material forms the foundation of your arbitration or civil claim to recover the amounts paid.

Key takeaways

The unconditional bank guarantee meaning is straightforward in practice: the bank pays the beneficiary on written demand alone, with no requirement to prove default. That single characteristic drives every risk your firm carries when you furnish one. Indian courts uphold these instruments firmly, agencies across GeM, CPPP, and state portals require them at every project stage, and the payment process moves forward regardless of any dispute you raise after a demand lands.

Your most reliable protection is disciplined project execution that keeps invocation off the table entirely. Beyond that, verify your BG format matches the prescribed annexure exactly, confirm your issuing bank is on the approved list, track both the validity date and the claim window deadline, and build a paper trail of performance throughout the contract lifecycle.

If you want a platform that flags BG clauses, qualification criteria, and unusual risk terms in tender documents automatically, explore what Arched can do for your BD team.