Canara Bank Bank Guarantee Charges 2026: Fees, Rates, GST

Master the 2026 canara bank bank guarantee charges to price your tenders accurately. Learn about commission rates, GST, and tips to reduce your financing costs.

Every government tender you bid on demands a bank guarantee, for earnest money, for performance security, or sometimes both. And the charges your bank levies on that guarantee directly eat into your project margins. If you're working with Canara Bank, understanding Canara Bank bank guarantee charges upfront is non-negotiable before you commit to a bid. Get this wrong, and a contract that looked profitable on paper starts bleeding money before mobilization even begins.

Canara Bank, one of India's largest public sector banks with deep roots in infrastructure and project financing, applies a structured fee model for issuing bank guarantees. This includes commission rates that vary by guarantee type and tenure, margin money requirements, and processing fees, all subject to GST. For contractors regularly bidding on government projects through platforms like GeM, CPPP, or state e-procurement portals, these costs add up fast. A firm bidding on five to ten tenders a month can easily spend lakhs annually on BG-related charges alone.

This is exactly where accurate bid-cost planning meets opportunity discovery. At Arched, our platform helps infrastructure firms and government contractors identify high-probability tenders across 500+ portals, but winning starts well before the bid submission. It starts with knowing your true cost of participation, and bank guarantee charges are a critical piece of that puzzle.

In this article, we break down Canara Bank's current bank guarantee fee structure for 2026, covering commission rates, margin requirements, renewal fees, and applicable GST. Whether you're a mid-sized contractor evaluating your first performance guarantee or a seasoned BD team optimizing bid costs across multiple projects, this guide gives you the exact numbers and context you need to plan with confidence.

Why bank guarantee charges matter in tenders

When you submit a bid for a government contract, bank guarantees are not optional. They are a condition of entry. The procuring department uses them to ensure you follow through on your commitment, whether that's entering into the contract after winning the bid or completing the work to specification once you do. For most government tenders in India, you'll need at least one BG, and often two: an Earnest Money Deposit (EMD) guarantee at the bid stage and a Performance Security guarantee after award. Each one carries charges, and those charges start accumulating the moment your bank issues the document.

Bank guarantees are a mandatory cost of participation

Every public tender issued under frameworks like the General Financial Rules (GFR) or state procurement rules requires bidders to furnish a BG or equivalent security. This applies whether you're bidding through GeM, CPPP, or any state e-procurement portal. The EMD typically runs between 1% and 2% of the estimated contract value, while performance security usually sits between 5% and 10% of the final contract value. On a Rs 10 crore project, that's Rs 10-20 lakh locked up as EMD and Rs 50-100 lakh tied up as performance security for the duration of the project.

Your bank charges commission on the guaranteed amount for each quarter or part thereof. Add to that the margin money your bank blocks, the processing fee, and GST at 18%, and the cost of holding a single BG on a medium-sized project can run into several lakhs over the project lifecycle. For firms bidding on multiple tenders simultaneously, these costs stack up quickly.

If you're not factoring BG charges into your bid cost calculations from day one, you're understating your cost of participation, which directly distorts your profitability projections.

How BG charges affect your actual project margins

Most contractors focus on direct costs: materials, labor, equipment, and overheads. Financing costs, including bank guarantee commissions, are often treated as a line item added at the end rather than modeled from the start. This is where many firms lose money without realizing it. A project with a 12% gross margin can see that figure compress significantly once you account for BG commissions across EMD, performance, and advance payment guarantees held over an 18-to-24-month execution period.

Consider a contractor managing five active projects simultaneously, each requiring performance security of Rs 50 lakh at a commission rate of 1.5% per annum. That's Rs 3.75 lakh per year in BG commissions alone, before GST. Scale that to larger contracts or longer tenures, and the figure grows fast. Understanding Canara Bank bank guarantee charges before you submit a bid lets you price your offer with full visibility into what it actually costs you to participate and deliver.

Accurate cost modeling also affects your go/no-go decision on a tender. If a contract offers thin margins and requires a large BG over an extended period, the financing cost may tip the deal from viable to unviable. Knowing the exact fee structure of your bank before you commit gives you the data to make that call clearly. This is not a back-office accounting concern. It's a front-end strategic input that belongs in every bid cost model your team builds.

What Canara Bank charges for a bank guarantee

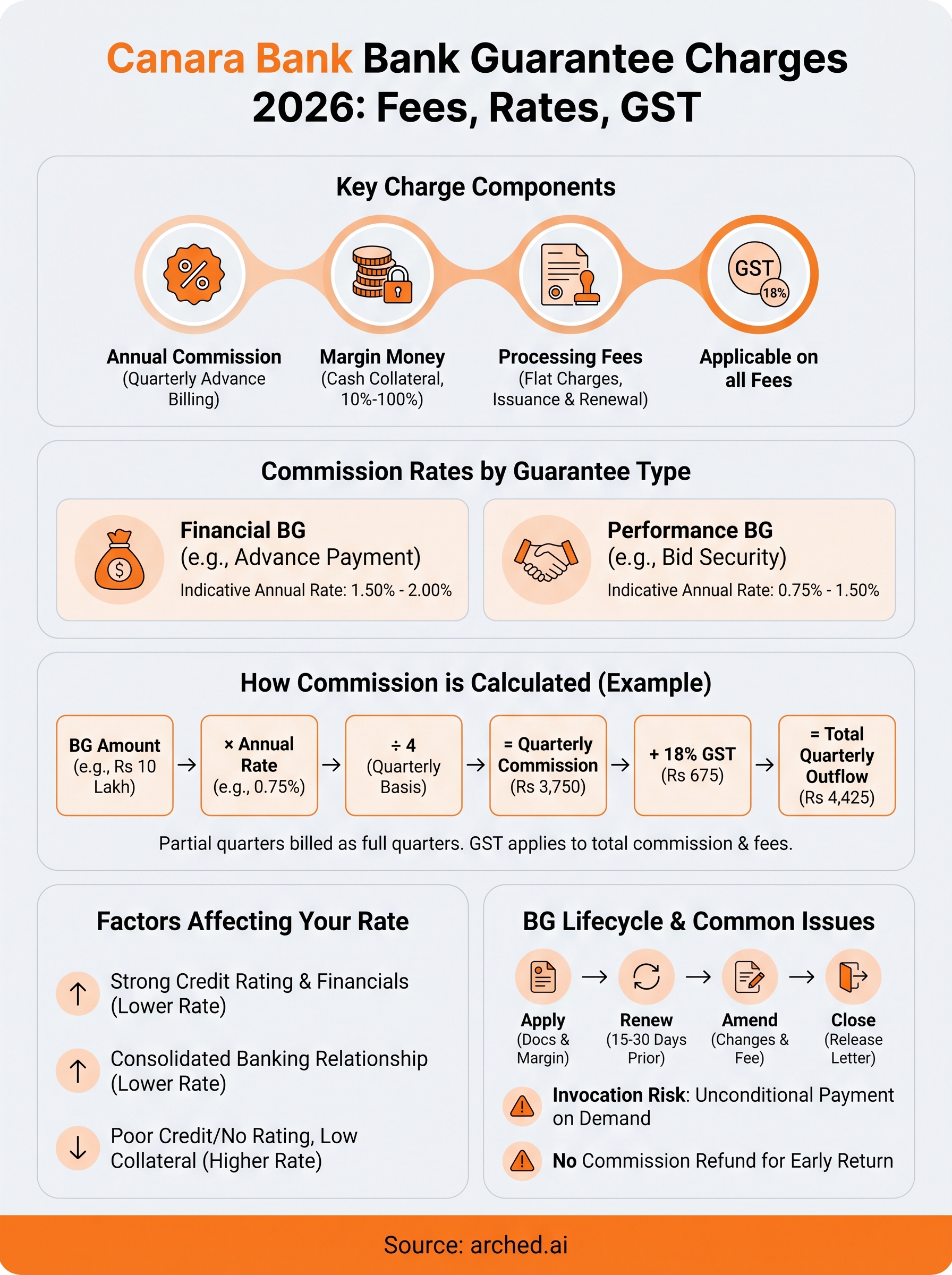

Canara Bank structures its bank guarantee charges across several distinct components. Understanding each one separately is the only way to arrive at your true cost of holding a BG for the duration of a tender or project. Lumping everything into a single estimate without breaking it down is how bid cost models go wrong.

Commission rates by guarantee type

The primary charge is the annual commission, calculated as a percentage of the guaranteed amount and billed quarterly in advance. Canara Bank applies different rates depending on whether the guarantee is a financial guarantee (such as an advance payment guarantee) or a performance guarantee (such as a bid security or contract performance security). Financial guarantees carry higher rates because they represent a direct monetary obligation, while performance guarantees are tied to contractual delivery.

| Guarantee Type | Indicative Annual Rate |

|---|---|

| Financial BG (advance payment, deferred payment) | 1.50% to 2.00% per annum |

| Performance BG (bid security, performance security) | 0.75% to 1.50% per annum |

These rates reflect Canara Bank's general published schedule; your actual rate depends on your credit rating, collateral offered, and the branch's assessment of your overall account relationship.

Additional charges: margin money, processing fees, and GST

Beyond commission, Canara Bank typically blocks margin money as cash collateral against the BG. This amount is not a fee you pay out, but it does lock up your working capital for the entire BG validity period. The margin percentage varies: rated borrowers with strong credit histories may deposit 10% to 25% of the BG value, while non-rated or first-time applicants can face requirements up to 100% cash margin.

Processing fees apply at the time of issuance and again at each renewal. These are flat charges that generally range from a few hundred to a few thousand rupees depending on the BG value and complexity. For amendments, such as extending the validity or increasing the guaranteed amount, Canara Bank levies a separate amendment fee. All commission, processing, and amendment charges are subject to GST at 18%, meaning your actual cash outflow is always 18% higher than the stated base rate. Build that into every bid cost model from day one.

How Canara Bank calculates BG commission with examples

Understanding the calculation method behind Canara Bank bank guarantee charges is essential before you commit to a bid. The bank does not charge a flat fee on the total contract value. Instead, it applies a quarterly commission on the face value of the guarantee, billed in advance at the start of each quarter or part thereof. That last phrase matters: even if your BG validity runs for, say, seven months, Canara Bank treats that as three full billing quarters, not 2.33.

The core commission formula

The standard approach Canara Bank uses to calculate commission is straightforward once you break it into its parts. You multiply the guaranteed amount by the applicable annual rate, then divide by four for each quarter, and bill that amount upfront. Any partial quarter counts as a full one, which means longer tenures and awkward end dates cost you proportionally more.

The formula works like this:

Quarterly commission = (BG Amount × Annual Rate) ÷ 4

For a BG running across multiple quarters, multiply the per-quarter figure by the total number of quarters (including any partial quarter). Then add GST at 18% on top of the total commission to arrive at your actual cash outflow.

Worked examples: EMD and performance security

Two BG types appear most often in government tenders: bid security for the EMD stage and performance security post-award. The table below shows how the commission math plays out at typical rates and tenures.

| BG Type | BG Amount | Annual Rate | Tenure | Base Commission | GST (18%) | Total Outflow |

|---|---|---|---|---|---|---|

| EMD / Bid Security | Rs 10 lakh | 0.75% | 6 months (2 qtrs) | Rs 3,750 | Rs 675 | Rs 4,425 |

| Performance Security | Rs 50 lakh | 1.50% | 24 months (8 qtrs) | Rs 1,50,000 | Rs 27,000 | Rs 1,77,000 |

| Advance Payment BG | Rs 25 lakh | 2.00% | 12 months (4 qtrs) | Rs 50,000 | Rs 9,000 | Rs 59,000 |

On a Rs 50 lakh performance security held for two years, your total financing cost crosses Rs 1.75 lakh before you've spent a single rupee on the project itself.

For any multi-BG bid, add each guarantee's total outflow separately. A contractor holding all three BG types above simultaneously would spend over Rs 2.4 lakh in financing charges before breaking ground, a figure that must sit inside your bid cost model, not outside it.

What affects your rate and how to lower the cost

Canara Bank does not apply a single fixed rate to every applicant. The commission rate you receive on a bank guarantee depends on a combination of financial and relationship factors that the branch assesses before issuing the instrument. Understanding what drives that rate puts you in a position to negotiate, rather than simply accept whatever the relationship manager quotes you.

Key factors that determine your commission rate

Your credit risk profile is the single biggest lever. Canara Bank assigns internal risk ratings to borrowers based on financial statements, repayment history, and existing credit limits. A firm with a strong credit rating, clean repayment record, and audited financials showing healthy turnover will consistently receive rates at the lower end of the published range. Firms without a formal credit rating, or those with irregular repayment patterns, face higher rates and steeper margin requirements.

The size of your overall banking relationship also matters. If Canara Bank holds your primary current account, your term loans, and your working capital limits, you carry more negotiating weight than a contractor who approaches the bank purely for a one-off BG. Banks price relationship value into their guarantee rates, even if that is rarely stated explicitly.

The more consolidated your banking activity at one branch, the more leverage you have to push your Canara Bank bank guarantee charges toward the lower end of their rate band.

Practical steps to reduce your BG cost

Several concrete actions can reduce what you pay on each guarantee. Submitting complete, audited financials at the start of every financial year rather than waiting until a BG request forces the issue means the branch already has a current file on you. That speeds up processing and strengthens your credit assessment. Similarly, offering higher-quality collateral, such as fixed deposits or property rather than personal guarantees, typically reduces both the margin requirement and the applicable rate.

You should also consider consolidating multiple small BG requirements into fewer instruments where the tender terms permit. A single larger guarantee often attracts a marginally better rate than several small ones, and it reduces the number of processing fees you pay. Finally, negotiating a pre-approved BG limit as part of your annual credit review eliminates the need for fresh appraisals on every tender, cutting both turnaround time and incidental charges.

How to apply, renew, amend, and close a BG

The lifecycle of a bank guarantee runs from initial application through to eventual closure, and each stage carries its own documentation, timelines, and charges. Knowing this lifecycle in advance prevents last-minute surprises on submission deadlines or renewal windows that could put your contract at risk.

Applying for a bank guarantee

Your first step is submitting an application form along with a set of supporting documents to your Canara Bank branch. Standard requirements include the tender notice or award letter specifying the BG format, your firm's audited financial statements for the last two to three years, KYC documents, and the applicable margin money. If you already hold a pre-approved BG limit under your working capital facility, processing is significantly faster, often within one to three working days. Without a pre-approved limit, fresh appraisal can take a week or longer depending on branch workload.

Carrying a copy of the BG format prescribed in the tender document to the branch, rather than asking them to draft one independently, avoids wording disputes and cuts turnaround time. Confirm that the format satisfies the procuring department before you submit, since revisions after issuance attract amendment charges that add to your overall Canara Bank bank guarantee charges.

Renewing, amending, and closing your BG

Renewal is required when your project timeline extends beyond the original BG validity. Submit a renewal request at least 15 to 30 days before expiry to avoid a lapse in coverage. A lapsed BG can trigger invocation by the beneficiary department, which is both financially damaging and harmful to your firm's track record. Canara Bank charges the standard quarterly commission on the extended period, plus GST, along with a processing fee for the renewal instrument.

Always calendar your BG expiry dates at the point of issuance, not when a renewal reminder lands on your desk.

Amendments cover changes to the guaranteed amount, validity period, or beneficiary details. Each amendment requires a formal written request, the original BG document, and payment of the applicable fee plus GST at 18%. Closure happens once the beneficiary formally releases the guarantee after project completion or bid withdrawal. Submit the original BG document and a release letter from the department to your Canara Bank branch, and the bank will return any margin money held against that instrument once it confirms the release is valid.

Common issues, disputes, and FAQs

Even contractors who manage their BG lifecycle carefully run into problems. Understanding the most common friction points around Canara Bank bank guarantee charges before they happen lets you respond quickly rather than scrambling when a deadline or dispute lands on your desk.

When a BG gets invoked or threatened

Invocation happens when the beneficiary department claims you failed to meet your contractual obligations, whether that's not signing the contract after winning a bid or not completing the work to specification. Once a department sends a written demand to Canara Bank, the bank is obligated to honor the guarantee without investigating the underlying dispute. That is the nature of an unconditional BG.

If you believe an invocation is wrongful, your recourse is through the civil courts, not through the bank. Canara Bank will pay the beneficiary and then recover the amount from you.

Your best protection is preventing invocation by tracking project milestones, validity dates, and compliance requirements in real time. If a dispute with the department looks likely, address it formally in writing well before the BG expiry date.

Disputes over charges and how to resolve them

Overbilling on BG commission is more common than it should be. A branch may charge commission on a partial quarter at the full quarterly rate but then fail to apply the correct annual rate specified in your sanction letter. Always reconcile every debit against your sanction terms. If a discrepancy appears, submit a written complaint to the branch manager with a clear calculation showing the correct amount. Canara Bank's grievance process requires a response within 30 days.

Frequently asked questions

Can you get a refund on commission if you return the BG early? Generally, no. Canara Bank charges commission quarters in advance and does not refund unused periods if you return the instrument before the validity ends. Factor this into your tenure decisions upfront.

What happens if you miss the renewal deadline? A lapsed BG is treated as expired by the beneficiary department. The department may invoke it or reject your bid status entirely. Submit renewal requests at least three weeks before expiry to avoid this.

Does the margin money earn interest? If your margin is held as a fixed deposit, Canara Bank typically credits interest on that FD to your account, though the rate applied is the prevailing FD rate at the time of deposit, not the lending rate.

Next steps

You now have a complete picture of Canara Bank bank guarantee charges, from the commission rates and margin requirements to how billing works across quarters, what drives your rate, and how to manage renewals and disputes. The key takeaway is simple: treat BG costs as a front-end input in every bid model, not an afterthought reconciled at project close. When you know your exact financing costs before you submit, you bid with precision rather than assumption.

That discipline matters even more when you're evaluating a high volume of tenders across multiple portals. Missing a BG expiry, bidding on a contract where the financing costs eat your margin, or discovering after award that you're under-qualified are all avoidable mistakes with the right infrastructure in place. Arched helps government contractors do exactly that, matching your firm's actual credentials to viable tenders across 500+ portals. Explore what Arched can do for your BD pipeline and start bidding on the right contracts.